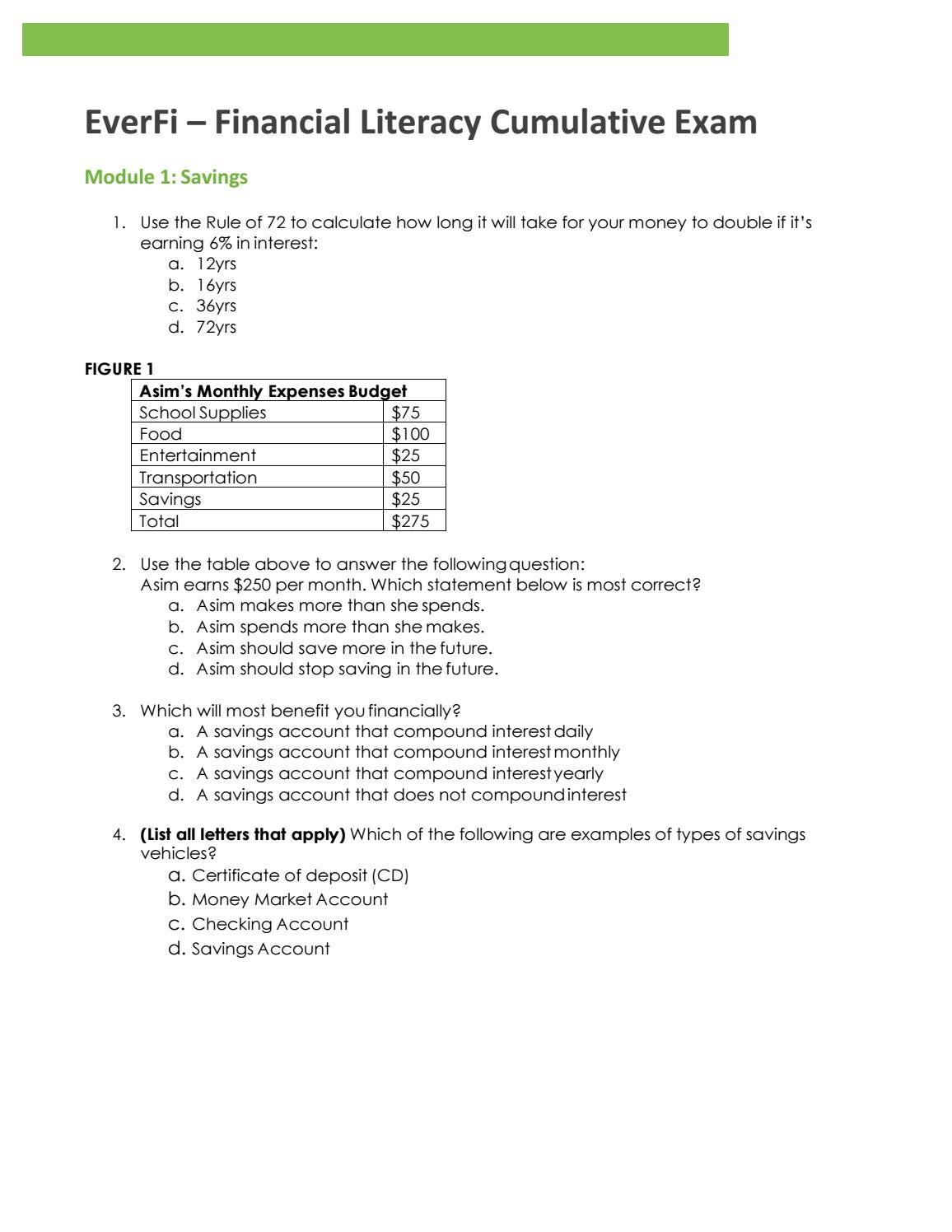

Get a free, zero duty personal loan price which have pricing as low as 9.99%

When you take out home financing to invest in property purchase, you ought to built area of the purchase price yourself. From inside the Canada, you desire no less than a good 5% downpayment when you purchase a house. But what from the the second domestic? Are definitely the lowest requirements additional?

There are lowest downpayment requirements purchasing a property from inside the Canada, should it be your first or 2nd domestic. The brand new advance payment required relies on the value of your property and you can whether it is an owner-occupied or non-owner-filled home:

Owner-Filled Property

Keep in mind that down payments lower than 20% will need CMHC insurance or mortgage standard insurance rates. These types of insurance protects the financial institution in the event that you stop and then make your own home loan repayments. Although not, house charged over $one million do not qualify for CMHC insurance rates. Yet not, active ortizations was open to first-time homebuyers or those people who are to shop for a recently built family.

Non-Manager Occupied House

Residential property that’ll not be occupied because of the homeowner and they are designed for rent objectives possess highest deposit conditions. Leasing attributes wanted the absolute minimum advance payment regarding 20%

Create note that off costs need to are from your savings, the selling of a house or as the a non-repayable current off a member of family.

Simply how much Try Financial Default Insurance coverage?

Home loan default insurance coverage vary from 0.6% to help you 4.0% of purchase price of the home. So it superior is typically folded to your mortgage payments, though you can decide to blow they initial in one single lump sum at closure.

Then, in case the home is located in Saskatchewan, Ontario, otherwise Quebec, you’ll need to shell out provincial taxation on advanced, hence should be repaid initial after you romantic to the home. This income tax can’t be rolling to your home loan.

You will find differences when considering buying an additional home, including a cottage, and you may an investment property that one may earn a revenue out-of. Listed below are some secret differences between both:

When you have sufficient security on your first residence, you can use it to place with the downpayment on an extra house. Within the Canada, you might obtain around 80% in your home equity, with no leftover financial equilibrium, with regards to the bank.

But not, dont one to CMHC-insured mortgages do not let borrowed money because an advance payment. To make use of your property security, you have you work at private financial standard insurance providers such Sagen and you can Canada Guaranty.

Family Equity Mortgage

Domestic security loans is versatile, to help you utilize the loans for assorted aim, also for an advance payment towards a moment domestic. With this particular loan, you can borrow doing 80% of your own home’s guarantee.

Eg a routine loan, you’re going to get a lump sum payment of money, that you’ll need to repay through installments more than a set identity. Your home protects the borrowed funds, it is therefore crucial that you keep up with your repayments to avoid the possibility of having your family caught on account of financing default.

Family Equity Line of credit (HELOC)

Good HELOC functions such as for instance a consistent line of credit, but your home backs the mortgage. Having a beneficial HELOC, you have access to up to 65% of your home’s equity. In the place of a home guarantee mortgage, you could withdraw funds when you need all of them, and you may attract are energized just into the number taken. After that you can make use of the finance to get on a down percentage into the a moment house.

Cash-Away Refinance

A finances-away refinance is yet another solution to availability your residence’s equity. Having a routine re-finance, you might pull out a different financial to restore your current you to, always which have the new terminology and you will another rates. That have an earnings-out refinance, particularly, you’d re-finance the mortgage for over what exactly is however kept on your mortgage equilibrium, right after which make difference between bucks.

Exactly what do You need to Be considered In order to Borrow secured on Your House’s Equity?

To-be permitted borrow against your property security, you can easily generally speaking you would like at least 20% guarantee of your house. With regards to the lender, it’s also possible to you desire a top credit history and you will a lower debt-to-income (DTI) ratio.

In this situation, you have finest chance coping with an alternative financial. That have Alpine Loans, you can nonetheless be eligible for a property guarantee mortgage even with bad credit and low income, as more interest is positioned on the collateral you have into the your cash advance Banks Banks, AL house than your financial and credit reputation.

Just how much In the event that you Budget for The second Household?

Casing charges for one minute household are similar to what you’d buy the majority of your quarters. Since the direct will set you back tends to be slightly highest or below what you’re buying very first house, the costs try seemingly equivalent:

Closing costs

When you first get a property, you will need a lump sum of money to fund closing costs before you take hands of the home, that range from the adopting the:

- Deposit

- Home loan standard insurance

- House import taxation

- Title insurance premiums

- Family inspection charge

- Judge charges

- Assessment fees

- Power setup and you will installment fees

- Home improvements

Closing costs range between 1.5% to help you cuatro% of the cost. Thus, eg, if your next household you are to find can cost you $500,000, you will have to plan for approximately $seven,500 to $20,000 upfront.

Ongoing Repair

Once you have off the beaten track the initial resource of the home get and you can settlement costs, there are plenty of costs associated with operating and you can keeping the new home:

The primary is to perform a detailed finances so you learn simply how much money to order and getting a moment domestic tend to charge a fee. A resources also let you know how much cash you will have left over at all expenditures was indeed safeguarded to suit your 2nd domestic.